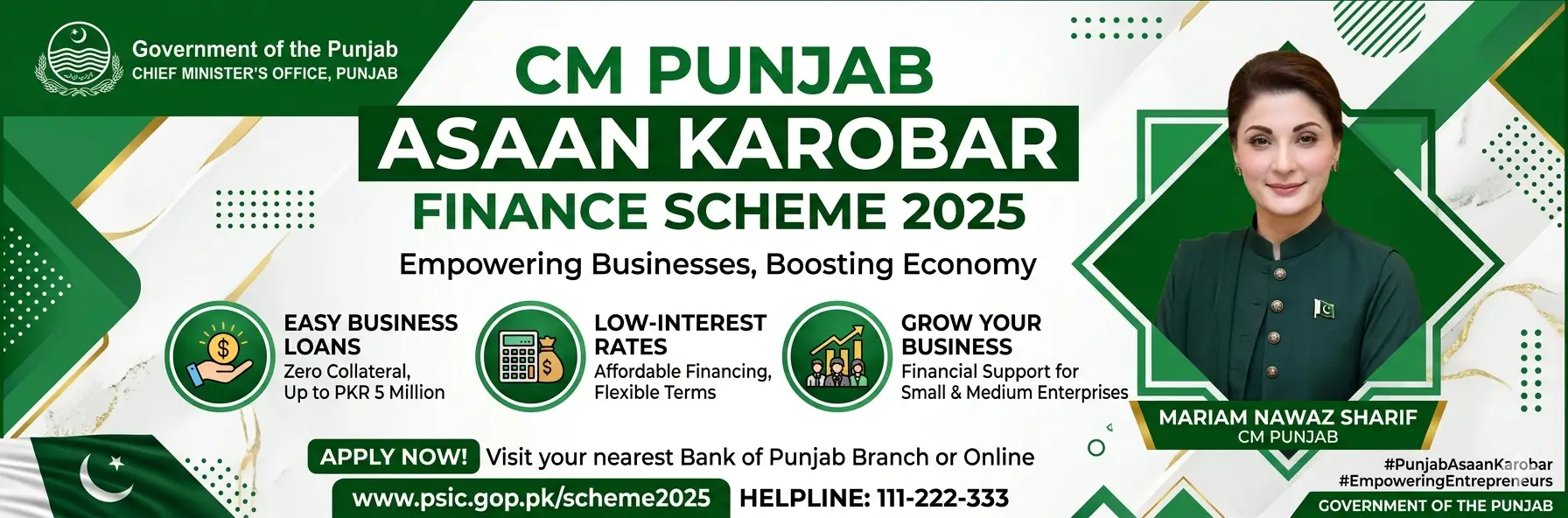

Small and medium-sized businesses have always been the backbone of Pakistan’s economy. Yet for millions of talented young people, one barrier has consistently held them back: a lack of startup capital. To close this gap, Chief Minister Punjab Maryam Nawaz Sharif launched the CM Punjab Asaan Karobar Finance Scheme 2025 — a landmark initiative designed to put affordable financing directly into the hands of Punjab’s entrepreneurs.

This isn’t just another government loan. It’s a comprehensive economic empowerment program that targets youth, women, and small business owners across the province. Whether you want to start a new venture or scale an existing one, this scheme could be the turning point you’ve been waiting for.

In this complete guide, we cover everything — what the scheme is, who qualifies, how much you can borrow, what documents you need, and exactly how to apply online step by step.

⚡ Quick Facts at a Glance

| Loan Limit | PKR 1 Lakh to PKR 30 Lakh |

| Markup / Interest Rate | Only 8% per annum (after government subsidy) |

| Loan Duration | Up to 3 years (extendable) |

| Grace Period | 6 months (no installment in first 6 months) |

| Age Eligibility | 21 to 57 years |

| Application Fee | Zero — completely free |

| Implementing Bank | Bank of Punjab (BOP) |

| Scheme Launch | January 2025 |

Scheme Overview — What Is the Asaan Karobar Finance Scheme?

The CM Punjab Asaan Karobar Finance Scheme 2025 is a government-backed SME financing initiative implemented through the Bank of Punjab (BOP). It provides low-cost loans to small and medium enterprises (SMEs) across Punjab with the aim of reducing unemployment, promoting self-employment, and energizing the province’s economy.

The scheme was announced at the beginning of 2025 as part of the Punjab Government’s broader agenda to boost economic activity at the grassroots level. The target is to create hundreds of thousands of new jobs and support existing businesses in expanding their operations.

The government covers a substantial portion of the markup through a subsidy, making borrowing costs far lower than anything available on the open market. This public-private partnership (PPP) model — with BOP as the financial partner and the provincial government as the guarantor — makes the scheme both credible and sustainable.

Objectives of the Scheme

- Provide affordable financing to small and medium-sized businesses across Punjab

- Cultivate an entrepreneurship culture among youth and women

- Reduce unemployment by creating new jobs through business growth

- Bring informal businesses into the formal, documented economy

- Expand the provincial tax base by encouraging new business registrations

- Empower women entrepreneurs through preferential access to loans

- Stimulate industrial and commercial investment at the district level

Key Features of the Asaan Karobar Finance Scheme

Loan Amount

Applicants can borrow a minimum of PKR 1 lakh and a maximum of PKR 30 lakh. The exact amount approved depends on the nature of the business, the applicant’s creditworthiness, and the projected financial need outlined in the business plan.

Markup Rate

Thanks to the Punjab Government’s subsidy, the effective markup rate is just 8% per annum. For comparison, commercial bank lending rates in Pakistan currently range from 16% to 22%. This difference alone can save a borrower several lakhs in financing costs over the loan term.

Repayment Period

The standard repayment period is three years, with installments structured to match the cash flow of a growing small business. In genuine hardship cases, a tenure extension may be considered by the bank.

Grace Period

One of the standout features of this scheme is the six-month grace period from the date of disbursement. During these six months, no installment is due. This gives the borrower time to set up the business, generate revenue, and then comfortably begin repaying — a critical feature that most commercial loans do not offer.

No Application Fee

The entire application process is completely free of charge. There are no processing fees, administrative charges, or hidden costs. This ensures that even the most financially constrained applicants can participate without hesitation.

Eligibility Criteria — Who Can Apply?

📌 Important: Before submitting your application, make sure you meet all of the following requirements. An incomplete or ineligible application will be rejected at the initial screening stage.

- Must be a permanent resident of Punjab province

- Age must be between 21 and 57 years at the time of application

- Must hold a valid Pakistani CNIC

- Must be a registered active tax filer with FBR (NTN required)

- Must have a clean credit history — no bank defaults or blacklistings

- Must not have an existing government loan outstanding

- Must have a viable business plan, or an already-operating business

- Women entrepreneurs will receive preferential consideration

- Both new startups and existing businesses are eligible

Required Documents — Complete Checklist

- Copy of CNIC (applicant and guarantor, if applicable)

- NTN Certificate (National Tax Number) from FBR

- Bank statement for the last 6 months

- Proof of residence — utility bill (electricity/gas) or rental agreement

- Business address proof (if business is already operational)

- A well-prepared Business Plan outlining objectives, financials, and use of funds

- 2 recent passport-size photographs

- Affidavit confirming no outstanding government loan

- For married women applicants: Nikah Nama (marriage certificate)

💡 Pro Tip: Scan all documents clearly before starting your online application. Blurry or incomplete uploads are one of the most common reasons for early rejection.

Loan Categories — Small & Medium Business

Small Business Loan (PKR 1 Lakh – PKR 10 Lakh)

This category is designed for individuals looking to start or grow a small-scale operation. It covers shopkeepers, cottage industries, skilled artisans, home-based businesses, and small agricultural support services. This is the most popular tier, attracting the highest number of applications, and is particularly well-suited for first-time borrowers.

Medium Business Loan (PKR 10 Lakh – PKR 30 Lakh)

This tier is aimed at entrepreneurs who already have an operating business and want to expand it. Eligible businesses include processing factories, e-commerce stores, import/export firms, logistics companies, and service-sector enterprises. Applicants in this category are expected to provide stronger documentation and a more detailed financial projection in their business plan.

How to Apply — Step-by-Step Application Guide

Applying for the Asaan Karobar Finance Scheme is straightforward. Follow these steps carefully to avoid delays or rejection:

Online Registration Guide

The entire registration process is digital, designed to be accessible from any smartphone or computer. Navigate to the portal at asaankarobar.punjab.gov.pk and click the “Apply Now” button on the homepage.

Enter your mobile number, confirm via OTP, and set a password for your account. The form itself is divided into clearly labeled sections and typically takes 20 to 30 minutes to complete if all your documents are ready. A save-and-continue feature allows you to finish in multiple sittings if needed.

After submission, you can log back in at any time to track your application status, respond to bank queries, or upload additional documents if requested.

Government & Bank Involvement

The Bank of Punjab (BOP) is the sole implementing financial institution for this scheme. It handles all aspects of the loan process — application screening, credit assessment, field verification, approval decisions, and repayment management.

On the government side, the Punjab Government provides the markup subsidy that brings borrowing costs down to 8%. The Punjab Small Industries Corporation (PSIC) and the Department of Industries, Commerce and Investment provide technical guidance and business development support to selected applicants.

A credit guarantee mechanism also protects the bank against default risk, which encourages BOP to approve a higher volume of loans than it would under purely commercial criteria. This government backstop is key to why the scheme can reach borrowers who might otherwise be considered too high-risk by conventional lenders.

Benefits for Youth & Entrepreneurs

- ✅ Affordable financing — markup rate at least 50% below the commercial market rate

- ✅ Six-month grace period — no repayment pressure while the business gets established

- ✅ Fully digital process — apply from home without standing in queues

- ✅ Preferential treatment for women — easier conditions and priority processing

- ✅ Free business training — selected applicants receive complimentary entrepreneurship workshops

- ✅ Transparent system — digital tracking eliminates bribery and favoritism

- ✅ Flexible repayment — monthly installment schedule matched to your business cycle

- ✅ Zero application fee — no upfront cost to apply

- ✅ Job creation — every loan-funded business creates employment in the community

- ✅ Open to new and existing businesses — startups and scaling businesses both qualify

Real-Life Use Cases — Who Benefits Most?

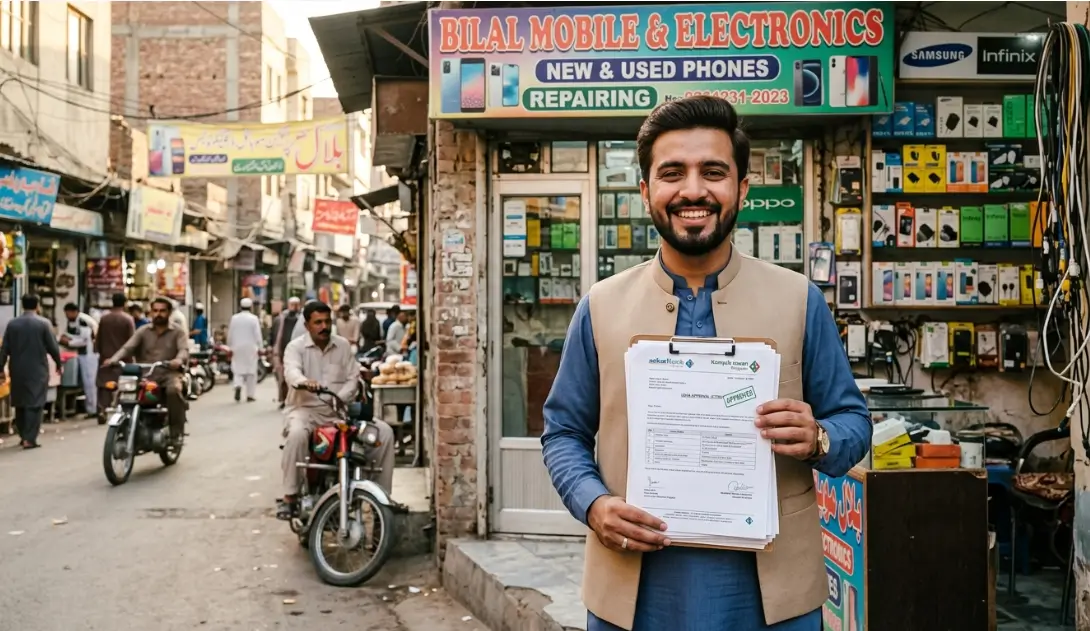

Adnan Khan, a resident of Lahore, used a PKR 5 lakh loan to open a general store in his neighborhood. The six-month grace period gave him time to build a customer base. He now repays comfortable monthly installments, supports his family, and employs two local young men.

Sana Rana from Faisalabad took a PKR 3 lakh loan to purchase a laptop, high-speed internet, and graphic design software. Today she earns in dollars through Upwork and Fiverr, easily covering her monthly installments while building a growing online business.

Bilal Ahmed, a young engineer from Multan, secured a PKR 20 lakh loan and launched an agricultural machinery repair and servicing company. Within one year, his startup turned profitable — providing cheap maintenance services to local farmers and creating new rural employment.

Common Mistakes to Avoid

- ❌ Submitting incomplete documents — this is the #1 reason for rejection at the initial stage

- ❌ Providing incorrect information — the bank verifies everything; inaccuracies lead to disqualification

- ❌ Not being a tax filer — register for NTN at FBR’s portal before applying; it is a hard requirement

- ❌ Applying without a business plan — a vague or missing business plan kills your application

- ❌ Missing installment payments — late payments damage your credit score and affect future borrowing

- ❌ Submitting multiple applications — duplicate submissions trigger automatic rejection flags in the system

- ❌ Uploading blurry document scans — always upload high-resolution, clearly legible copies

Approval Process & Timeline

The loan approval follows a structured, multi-stage process to ensure fairness and due diligence:

In total, the entire process from application to disbursement takes approximately 30 to 45 working days, provided all documents are complete and correct from the outset. Delays are almost always caused by incomplete documentation or difficulty reaching the applicant for the field visit.

Frequently Asked Questions (FAQs)

Q1. Who can apply for the Asaan Karobar Finance Scheme 2025?

Any permanent resident of Punjab aged between 21 and 57, holding a valid CNIC and active tax filer status (NTN), with no existing government loan default or bank blacklisting, can apply. Both new entrepreneurs and existing business owners are welcome.

Q2. Is this loan interest-free?

Not completely — but it’s close. The Punjab Government’s subsidy reduces the markup rate to just 8% per annum, compared to commercial rates of 16–22%. The government absorbs the difference, making it one of the most affordable loan products available in Pakistan today.

Q3. How long does it take to get approved?

After submitting a fully complete application with all required documents, approval and disbursement typically takes 30 to 45 working days. The most common cause of delay is incomplete documentation, so make sure everything is in order before you apply.

Q4. What documents do I need?

You need: CNIC copy, NTN certificate, 6-month bank statement, proof of residence, business plan, 2 passport-size photos, and an affidavit confirming no outstanding government loan. Married women also need to provide their Nikah Nama.

Q5. Can students apply for this scheme?

Yes! Students aged 21 or above who are permanent residents of Punjab, registered as active tax filers, and have a credible business idea with a documented plan are fully eligible. The scheme does not require you to have a currently operating business.

Q6. Is this scheme available outside Punjab?

No. The CM Punjab Asaan Karobar Finance Scheme is specifically for Punjab province residents. Applicants from other provinces should explore their own provincial programs — such as Sindh’s Youth Entrepreneurship Scheme or KP’s similar initiatives.

Your Business Dream Is One Application Away

The CM Punjab Asaan Karobar Finance Scheme 2025 is one of the most significant economic empowerment initiatives in Pakistan’s recent history. Funds are limited, seats are being filled fast, and this opportunity will not last forever. Don’t let the moment pass.

Gather your documents today, register on the portal, and take the first step toward building the business you’ve always envisioned.